The Weekly Random Walk – November 6, 2023 From Stephen Colavito

An Aggregation of Various Economic, Market Research, and Data

Transition

Transition – noun – the process of changing from one state or condition to another.

We view the word “transition” as the key to our world. It is a world with a diverse economy, wildly different political views, social and physical conflict, and markets trying to digest this over time.

This could be our most significant update of the year for various reasons. This week, we will try to lay the groundwork for what we could face in 2024. It will also be a “call to arms” about investing and the time needed to develop a thesis. In a world full of Tic Toks and 30-second soundbites, investors have grown impatient with market cycles and the time required to see assets appreciate.

— Transitions are never smooth.

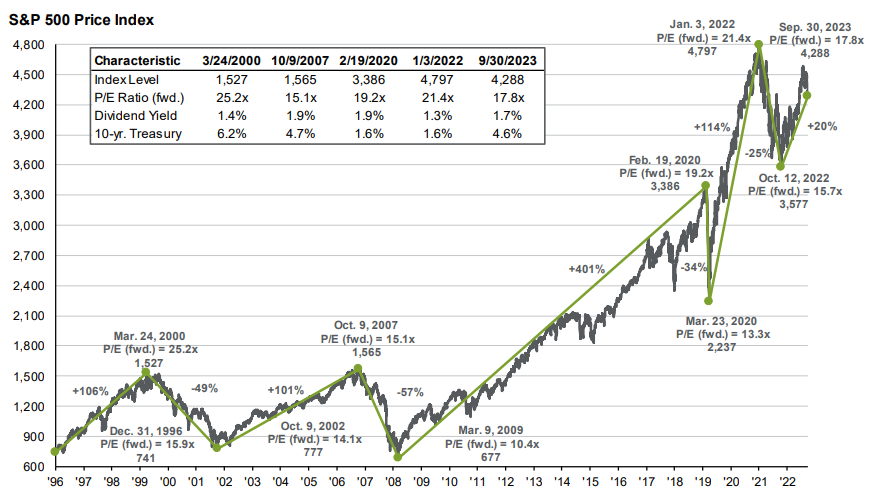

The chart below is a reminder that markets go up and down. But over time (this chart from JPM goes back to 1996), the market trend is higher.

Looking at the characteristics of the S&P 500 (price-weighted) Index, the P/E ratio is currently at 17.8x earnings, and the dividend yield is towards the higher end of the mean since 2000. This index is down for three months following valuation compression with higher yields. With the FOMC signaling that Fed Fund increases “may” be done, markets should see stabilization to this compression.

The most crucial point is this: investors are likely to lose if you try to time the ups and downs in the market. This chart includes several wars (Iraq and Afghanistan). So long as the conflicts remain geographically isolated and oil stays below $110 per barrel, the economy should remain somewhat stable (slight recession or slow growth). Generally, the cyclical conditions would play out as they usually do.

— Transition in interest rates (from low to high)

One of the most significant transitions was a Fed Fund at zero, moving up to north of 5% in a little less than two years. However, research from Deutsche Bank that builds a proxy of Fed Fund rates based on financial conditions (in addition to home prices) shows the effective Fed Fund rate to be close to two percent (200 bps) above the current target or in a range of 7.25-7.50%. Not surprisingly, the largest contribution to the increase in this proxy in recent months has been the surge in 10Y UST yields.

This +7% proxy is also in a model developed by the San Francisco Fed.

— Higher rates are transitioning to the economy, and things are slowing.

Higher interest rates are taking their toll on various sectors of the economy and market. The latest victims are mortgage REITs, which buy and fund agency and/or non-agency mortgages. Wider mortgage spreads, rising rates, and a flat yield curve hit net asset values and profitability. iShares Mortgage REIT ETF (REM) has shed 14.5% in October alone! While constituents like AGNC and Annaly Capital have dropped south of 25%. Lured in by juicy dividend yields, investors have turned to the asset class for supplemental income in recent years.

One should not be surprised at the consequence of zero rates or 4 trillion dollars of printed money. This is simple cause and effect. This means asset transition and revalue.

— Higher rates transition bond prices (yields up, prices down)

The journey from “lower for longer” proved painful for long-duration bondholders over the last 18 months. Now that the Fed appears to be done raising rates (for now), real bond returns could be positive for the next few years.

Bond yields reset swiftly, but it may take longer for the broader financial system to adjust to higher rates. We predict some turbulence in the lower credit quality segments (high-yield), mainly where business models rely on cheap financing. The investment-grade corporate paper seems to be in better shape, and we don’t feel refinancing creates much stress on this segment.

We continue to like three-year duration fixed income portfolios. Despite what we think is a pause in higher rates (and potentially lower rates this time next year), in the longer term, we are still concerned about a Government debt spiral that could rear its head with the continued excess spending out of Washington.

— Earnings are transitioning too.

We are now at the halfway point of the Q3 results for the S&P 500, and so far, earnings per share (EPS) have increased approximately 12% year-over-year (YOY), which is a 4% surprise to the upside. These gains have been led by utilities, discretionary, and communication services companies. Generally, this would have led to a rally, but corporations that beat EPS rallied a modest 1%, while those that missed their numbers fell about 2.5% (on average). The overriding theme so far is that very few companies are projecting a continued rise in EPS, with concerns that consumer spending may slow in the coming quarters combined with broad inflationary pressures (a.k.a. stagflation).

Several Wall Street firms have lowered their equity forecast as valuation support shrinks for stocks over the next six months while headwinds from elevated margins remain. Secondly, as we have reported several times, indices (S&P 500 and Nasdaq) have become overly concentrated in the technology sector. The recent pullback in markets has been led by some of the “high-flyers” earlier in the year. Markets will be susceptible to higher volatility (higher VIX) as markets transition past higher interest rates and lower forward guidance. We continue to like alternative investments as part of an allocation (for qualified investors) as a potential hedge against cyclical drawdowns.

The first chart below shows earnings which have been OK. The second chart shows demand worries at record highs. If companies are right, they may struggle to hit their numbers in early 2024.

— The transitioning workforce is hurting commercial real estate.

Commercial real estate building owners face significant headwinds as they try to refinance maturing loans in an environment of higher rates and tightening credit conditions. New data reveals more rumblings in the commercial-backed securities (CMBS) market, as well as a “deep freeze” spreading across the CRE space.

As employers navigate if employees should work from home or at the office, they continue to reduce their footprint to save on unnecessary expenses. A new report from the real estate company Treep shows a significant surge in industrial CMBS delinquency rates. This spike is in addition to rising delinquency rates as building owners lose long-term lease options and debt service coverage.

Blackstone’s Real Estate Income Trust (BREIT) has limited investor redemptions for the 12th straight month as investors sought to pull 2.2 billion of the funds' 66 billion real estate holdings. From our perspective, we are seeing “vulture funds” look to raise capital similar to what we saw in 2008-2009 to buy assets at “pennies on the dollar.” This is pretty typical when retail and fast money look for the exits after the damage has already been done.

— Transition Summary

Investors have become accustomed to double-digit returns with very little in the way of volatility. This was mainly due to a zero interest rate Fed policy and money printing/spending by Washington. Over the last 18 months, the transition of higher rate policy has taken place, but we continue to see money printing/spending from Washington; this has subdued some of the volatility in markets, but we believe it has prolonged the potential for an opportunity trade.

Over the next 5-10 years, we believe that we face the challenges of a world in transition. We think BRICS versus the dollar/SWIFT, global conflict because of tyrannical or lack of leadership, a fight over fossil versus alternative energy (or combination), real dollars or Central Bank Digital Currency (CBDC), etc. All will test the resolve of nations, economies, and markets.

But with transitions, investors have the opportunity to build portfolios that are robust (in real terms) to these challenges. Moving from disinflation to two-sided inflation risk and from policy accommodation to higher cost of capital means investors should insulate portfolios against more than just growth shocks. At the same time, themes relating mainly to the energy transition (or fight) and technology adoption will be necessary.

Even though the traditional 60/40 portfolio has faced headwinds over the last 18 months, it has been a successful balanced allocation for many years. However, building more intelligent portfolios for a world in transition demands that investors expand their portfolios into alternatives (for those who qualify) or even look toward specific international opportunities. It also means more of an active role by advisors and investors versus the passive way of investing, which has worked for many years. Tactical allocations and active rebalancing could be favorable to providing alpha in what may prove to be changing markets.

We encourage advisors and investors to take (not a 10-month view) but a 10-year view of investments. Investors should be reminded that in the 1970s, the last time we saw a global transition similar to what we face today, markets didn’t go straight up but bounced around wildly, causing heartburn for investors. But those who stayed the course made money and were better for it.

For those that don’t remember, here were the Dow Jones Industrial Average Returns in the 1970s:

1970: +4.82%

1971: +6.11%

1972: +14.58%

1973: -16.58%

1974: -27.57%

1975: +38.32%

1976: +17.86%

1977: -17.27%

1978: -3.15%

1979: +4.19%

As we said at the beginning of this piece…” transitions are never smooth.”

— This and That (Bullets)

Lastly, here are some interesting tidbits during the week that we think you’ll find interesting:

Those who love McDonald’s will not be happy with their meals (yep, we went there), as the company revenue was up 14% in the quarter in, which the burger company attributed to “strategic menu price increases (a.k.a. inflation). The company didn’t say which items had increased; however, it was reported that one branch in Darien, CT, charges as much as $18 for a Big Mac Combo (lots of special sauce) Meal! Go to Times Square, and you’ll pay $14.00. So much for cheap fast food. After the announcement, the Babylon Bee hit a 450-foot homerun when they tweeted a picture of a sign outside of a McDonald’s showing 0% Interest Financing For 36 Months on a meal. Brilliant!

In our prior life, we were censored about writing about ESG. Our position has always been it’s a noble cause, but Wall Street always finds a way to market and make money on nobility. So, in reporting “balls and strikes,” we highlight a Morningstar Report (a pro-ESG firm) highlighting that sustainable inflows into US ESG funds continue to fall but remain slightly positive. Simultaneously, the global mutual fund and ETF sectors of EGS experienced outflows. Morningstar blamed it on inflation and interest rates versus a gap in return versus non-ESG funds (which we predicted in 2022). Companies like InBev and Disney are two great examples of ESG (social governance) gone wrong, and investors have punished the stocks for the miscalculation.

In another “what are they thinking” (or are they thinking) moment, the White House announced last Thursday that it would indefinitely postpone a significant oil and gas lease sale mandated by the Inflation Reduction Act they promoted into law. The delay in Lease Sale 261, which spans almost 75 million acres across the Gulf of Mexico, was ordered on hold by the administration even though Judge James Cain of the Western District of Louisiana stated the White House proceed with Lease Sale 261. It makes no sense to us, with all of the uncertainty in the Middle East, why this administration continues to stop, delay, and deny energy independence. It’s just baffling.

Softer economic numbers have led to a nice short squeeze, helping the November rally get off to a good start. We believe 4500 is doable by year-end, particularly if the Fed passes again on raising rates in December. The range of 4200-4600 is still in place.

Trade carefully. Thank you for listening.

Have a great week.

Stephen Colavito

Chief Investment Officer

San Blas Securities

stephen.colavito@sanblas-advisory.com

General Disclosures

This research is for San Blas Clients only. The opinions represented in this research are that of the CIO, not advisors or officers of San Blas Securities. This research is based on current public information that we consider reliable, but we need to represent it as accurate and complete, and it should not be relied on as such. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate. Some research can and will be published irregularly as appropriate in the analyst’s judgment.

This research is not an offer to sell or solicitation of an offer to buy a security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or consider our clients' particular investment objectives, financial situations, or needs (individual or corporate). Clients should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including tax advice. Past performance is not a guide for future performance, future returns are not guaranteed, and a loss of original capital may occur. More information on San Blas Securities is available at www.sanblassecurities.com.